Where Has the Greenium Gone?

Filed in: Momentum |Investment |Pensions |Savings |Economy

26 March 2024

by Charles Thompson

A few years back a new word was added to the long list of bond market jargon: ‘greenium’. This comes from ‘green-premium’ but in fact represents a ‘green discount’ referring to the lower yield on bonds with positive ESG fundamentals compared to the equivalent bonds that do not.

This might sound straightforward, but a number of complexities arise. First is the verification that the proceeds of green bond sales are indeed allocated to worthy projects such as renewable energy or sustainable infrastructure.

Detailed frameworks exist to ensure compliance, such as the green bond principles from the International Capital Markets Association. Additionally, granular ESG scoring is available by entities such as ratings agency Moody’s and additional reassurance for investors is available from external audits by the large accounting firms.

Many of the sizable issuers in debt capital markets, such as the World Bank, have invested heavily in comprehensive and robust green bond frameworks. In fact, (1)all World Bank issues since 2021 have been part of their ‘sustainable development bonds and green bonds’ programme . In addition to the large multinational development agencies such as World Bank, EIB, Asian Development Bank and many others who are, by definition, funding projects with positive environmental or developmental impact, other corporate and government borrowers have also developed green bond programmes in recent years. This has been driven by investor demand and the opportunity for borrowers to fund at more competitive yield levels under green bond programmes.

A second consideration is to determine how much this positive ESG impact is worth from an investor standpoint. Here there could be a conflict when stated investment objectives of maximising fund return are combined with a target exposure to green bonds.

When the UK Government issued their first green Gilt in September 2021 (UK Treasury 0.875% 2033), the auction was very heavily oversubscribed with £100bn of bids for a £10bn issue size. The 0.87% yield to maturity was estimated to be 0.025% lower than the expected level for a conventional gilt at that time, saving the UK Treasury £28m over the life of the bond.

As well as benefiting the UK Treasury, (2)investors also made additional profits (at least in the near term) as changes to the ‘greenium’ caused these Gilts to outperform on a market value basis.

Measuring the 'greenium' impact

Measuring the ‘greenium’ for UK Gilts was complicated by the need for a yield curve model to adjust for the maturity difference between the green Gilt and neighbouring Gilts with similar maturities, a sort of ‘join-the-dots' which can be quite complex.

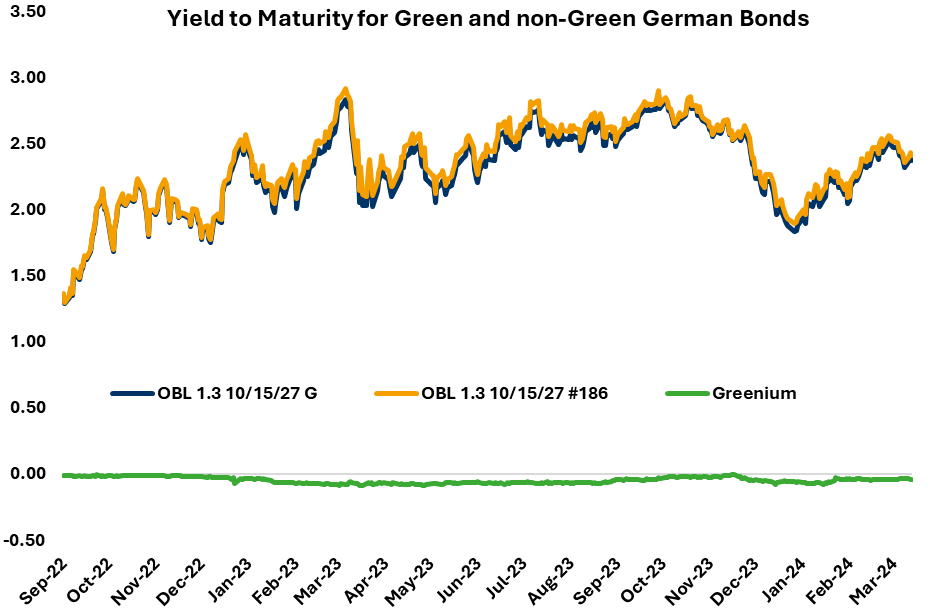

The German government has made things much simpler by issuing pairs of bonds, one green bond and one conventional, with precisely the same interest and principal payment dates and amounts.

Comparing the yield difference between these bonds gives an exact measure of the ‘greenium’. The following chart, using data from Bloomberg, shows the evolution of this ‘greenium’ for the German OBL 1.3% 2027.

Alarmingly, despite the additional ESG characteristics of the green OBL, not to mention the significant extra cost in managing and reporting within the green bond framework for the Federal Republic of Germany, their yield traded above the equivalent non-green issue. At that point the ‘greenium’ was negative, thus offering an ESG discount!

Fixed income investors often compare bonds with similar maturities to extract relative value. For example, by comparing the yield of a corporate bond to an equivalent maturity ‘risk free’ government bond, in the same currency, the so-called ‘credit spread’ can be determined.

‘Greenium’ is analogous to this credit spread but represents an altogether different measure. Buying a green bond with zero ‘greenium’ could be termed an ‘ESG arbitrage’ with future expected outperformance as the ‘greenium’ returns.

In conclusion, exposure to green bonds within a portfolio can contribute to benchmark outperformance as the relative valuations between green bonds and non-green bonds provide additional opportunities for active fixed income managers.

Sources:

- (1) The World Bank Sustainable Finance and ESG Advisory Services

- (2) The Financial Times