Site Search

Our site search facility enables you to look for content both within our main site and also our blog pages.

The first time a search is performed all pages are scraped for content which may take a few seconds to complete depending on your internet connectivity speed.

If you wish to search for a specific term or phrase please enable the 'ab' button within the search dialogue box

Expat Pension Planning

Insufficient retirement income is the major cause of financial stress

Recent surveys now document that retired “Baby Boomers” (individuals born in the years following the Second World War) are suffering bankruptcies in skyrocketing numbers. Although complex, these reports illustrate the simple fact that retirees do not have sufficient funds or income available - expat pension planning is designed to avoid these pitfalls.

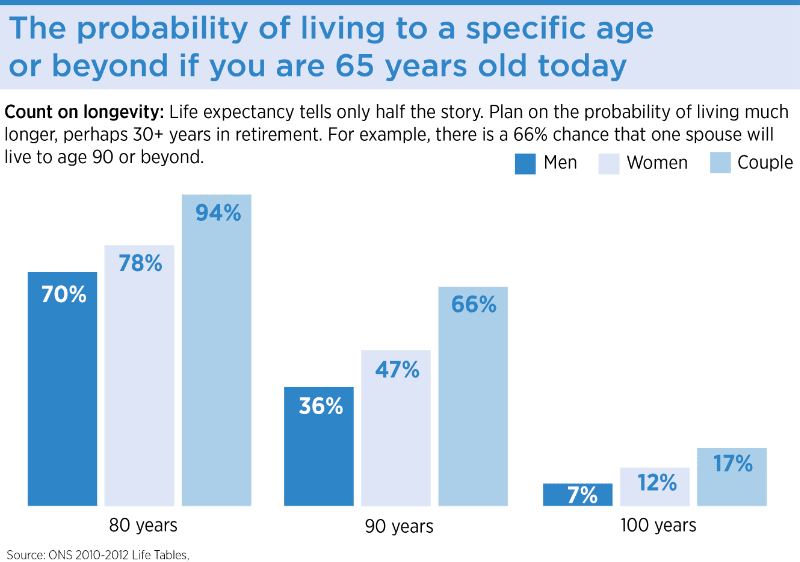

Life Longevity

If the elderly bankruptcy numbers were not sufficient evidence to illustrate the looming pension income problems for those in their twenty's, thirties, forties and even fifties we also learn that the vast majority of us are now living longer.

This chart illustrates the probability of living to a specific age or beyond if you are currently aged 65.

In conjunction with this data thought and consideration should also be given to the "Healthy life expectancy" factors.

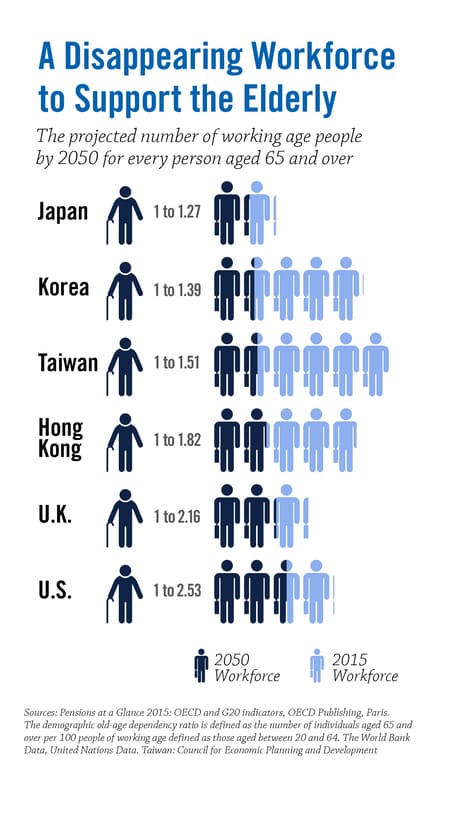

The disappearing workforce

Politics aside, Governments across the globe are continually reducing state and social benefits at every opportunity, the burden therefore to create personal retirement income streams is increasingly falling on the individual.

Group and company pension scheme arrangements do not fare much better, they too are under enormous stress.

Trends are now firmly established that confirm falling global workforces.

Should these trends continue, pension outcomes for those relying on such schemes may well fall short of what is expected today.

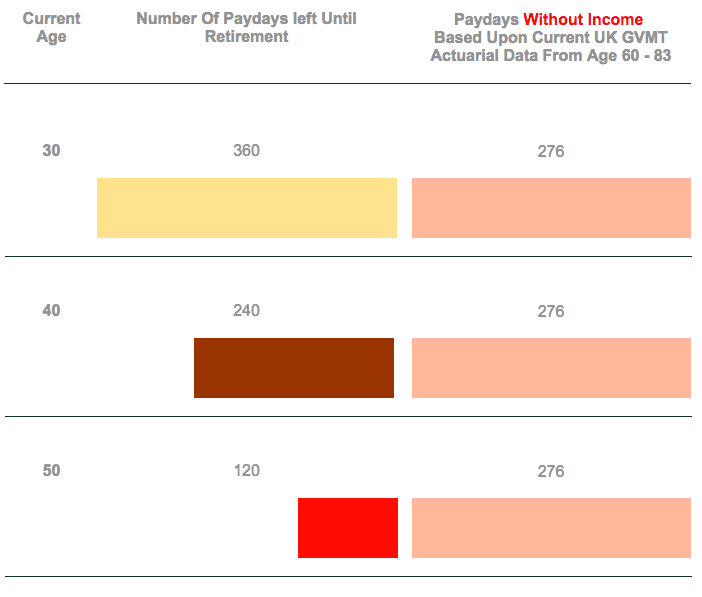

How many pay days left?

All too often we get wrapped up in our busy work and private lives and forget to realise how quickly time passes by. The number working days become less and less as we move forward, moving ever closer to our days in retirement.

Planning pension income has never been more important.

When looked at in this context you will come to understand that early planning action is essential if creating a liveable income when your working life comes to an end is important to you.

If you would like to read more about pension / retirement planning issues we have a number of informative pension articles here.