Site Search

Our site search facility enables you to look for content both within our main site and also our blog pages.

The first time a search is performed all pages are scraped for content which may take a few seconds to complete depending on your internet connectivity speed.

If you wish to search for a specific term or phrase please enable the 'ab' button within the search dialogue box

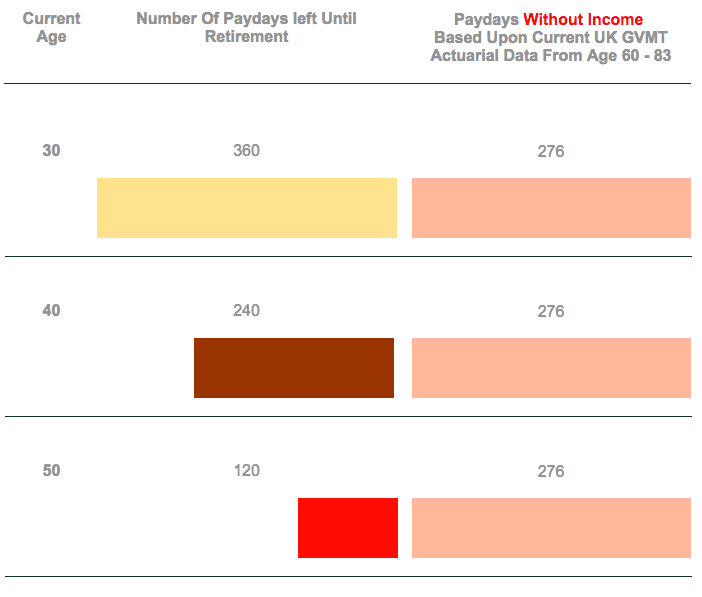

How Many Pay Days Left?

All too often our busy work and private lives prevent us from focusing on the important issues of pension and retirement planning, failing to recognise how quickly time passes us by until very often it is too late to make a meaningful impact on post work income.

It is a fact that the number of our working days diminish as we move forward, ever closer to our days in retirement meaning that our planning time has never been more important than now.

Governments around the world continue to extend our working lives in order to delay the payment of State benefits. In some parts of the world individuals need to reach age 70 before pension benefits from the state or company funded schemes become accessible. This is a trend likely to continue in the foreseeable future as those same Governments grapple with mounting debt.

Our expat pension planning page discusses the disappearing workforce and pensioner bankruptcy rates in more detail which should be alarming to all.

It is the case however that some people are happy to work until age 70 or beyond, but the vast majority of individuals we speak with are looking to scale back their working years in order to enjoy their retirement from a much younger retirement age - if you fall into this category you may well need to consider very carefully the retirement savings provision you are making if you are to attain the funds necessary to meet such goals.

You will find our pension related articles cover these issues in greater detail.

Early planning and action are therefore essential to create the income needed once the working life comes to an end.

Take a look at the graphical representation below of the paydays remaining for the various age groups: do you find these sobering facts?

Take action NOW to discuss YOUR options for securing YOUR retirement income.

The High Cost Of Procrastination in Retirement Planning

When it comes to retirement savings, time is truly money. The cost of delaying your retirement savings can be far more substantial than most people realize, due to one powerful financial force: compound interest.

Consider this sobering statistic from the U.S. Department of Labor: A 25-year-old who starts saving just $75 per month with an average annual return of 7% will accumulate approximately $227,000 by age 65. However, if that same individual waits until age 35 to begin saving, they would need to contribute $168 per month to reach the same goal - more than twice as much!

This phenomenon isn't just about losing potential interest earnings; it's about the exponential growth that occurs when returns generate their own returns.

The U.S. Securities and Exchange Commission refers to this as "the eighth wonder of the world" for retirement planning.

The Numbers Don't Lie: What Procrastination Really Costs

Let's put this into concrete numbers. Based on data from the US Financial Industry Regulatory Authority (FINRA):

• A 25-year-old who invests $5,000 annually until age 65 (40 years) with a 7% annual return would accumulate approximately $1,068,048

• A 35-year-old following the same investment strategy for 30 years would accumulate only $505,365

• A 45-year-old would accumulate just $228,810 over 20 years

That means waiting just 10 years (from age 25 to 35) cuts your retirement fund potential by more than half. Waiting 20 years reduces it by nearly 80%. These figures demonstrate the harsh financial reality of procrastination.

When Life Throws a Curve Ball: Health and Employment Disruptions

Planning for retirement becomes even more critical when considering the unexpected life events that can derail even the most carefully constructed plans. According to the U.S. Bureau of Labor Statistics, the average worker experiences about 12 job changes throughout their career, with periods of unemployment averaging 22 weeks for those 55 and older.

Health-Related Disruptions

The probability of experiencing a disability that prevents work increases dramatically as we age:

• At age 30, workers have a 21% chance of becoming disabled for 90 days or more before retirement

• By age 40, that risk increases to 25%

• By age 50, it reaches nearly 33%

Data from the Social Security Administration reveals that over 1 in 4 of today's 20-year-olds will become disabled before reaching retirement age. Moreover, the average long-term disability absence lasts 34.6 months--nearly three years during which retirement contributions often cease entirely.

When health issues force early retirement, the financial impact is twofold:

1. The savings period is cut short at a critical time when contributions are typically highest

2. The withdrawal period becomes longer, requiring the accumulated funds to stretch further

Unemployment's Double Penalty

Job loss creates a similar double-impact on retirement planning:

1. Immediate contribution loss: During periods of unemployment, retirement contributions typically stop completely

2. Early withdrawal temptation: Financial strain during unemployment often leads people to tap into retirement savings prematurely

According to the Employee Benefit Research Institute, about 40% of workers who experience an extended period of unemployment make early withdrawals from their retirement accounts. When factoring in early withdrawal penalties, income taxes, and lost compound growth, the true cost of a $10,000 early withdrawal at age 40 could exceed $100,000 in lost retirement funds by age 65.

The Early Bird Advantage: Starting Young Changes Everything

The flip side of this equation presents a much more optimistic picture. Starting early with retirement savings allows for:

• Lower monthly contribution requirements: Early savers can contribute less per month while still reaching the same goals

• Greater risk tolerance: Younger investors have more time to recover from market downturns, allowing for potentially higher-return investment strategies

• Financial flexibility: Building substantial early savings provides a cushion against those unexpected life events discussed above

The Remarkable Power of Starting Early

Government data from retirement studies reveals that a 22-year-old who invests just $3,000 annually for 10 years (total contribution: $30,000) and then stops completely--allowing the money to grow untouched until age 65--would accumulate more wealth than someone who waits until age 32 and then invests $3,000 annually for 33 straight years (total contribution: $99,000).

This counter-intuitive outcome demonstrates the extraordinary advantage that early savers have, even if they can only maintain their savings habit for a relatively short period.

The Psychological Benefits of Early Planning

Beyond the mathematical advantages, early retirement planning delivers significant psychological benefits:

• Reduced financial stress: Research by the American Psychological Association consistently shows that money concerns rank among the top sources of stress for adults

• Greater workplace satisfaction: Workers with secure retirement plans report higher job satisfaction and productivity

• Improved healthcare outcomes: Financial wellbeing correlates strongly with better health management decisions and outcomes

Action Steps - What You Can Do Starting Today

Regardless of your current age or financial situation, there are concrete steps you can take immediately to improve your retirement outlook:

For those under 30

• Start contributing to employer-sponsored retirement plans immediately, at least to the level of any employer match

• Establish automatic contribution increases that coincide with salary raises

• Consider allocating a higher percentage to growth investments, given your long time horizon

For those in Their 30's and 40's

• Maximise tax-advantaged retirement contributions whenever possible

• Review your portfolio allocation to ensure it aligns with your time horizon

• Create a catch-up plan if you've started late, potentially increasing your savings rate to 15-20% of income

For those in Their 50's and beyond

• Take advantage of catch-up contribution provisions in retirement accounts

• Reassess your planned retirement age and consider if working a few additional years might significantly improve your financial security

• Begin to shift some investments toward more conservative allocations to protect against market volatility as retirement approaches

For Everyone

• Create or update your retirement calculation, using realistic assumptions about inflation, investment returns, and longevity

• Consider working with a certified financial planner to optimise your strategy

• Review and adjust your plan annually as circumstances change

Conclusion: The Time to Act is Now

The mathematics of retirement planning are unforgiving. Delay carries a high cost, while early action delivers benefits that multiply over time. The difference between comfortable financial security and potential hardship in retirement often comes down to decisions made decades earlier.

Whether you're just beginning your career or can see retirement on the horizon, the most important step is to take action now. Even small initial contributions, consistently maintained and gradually increased, can grow into the foundation of a secure and dignified retirement.

Remember: Every day that passes is one fewer payday left to build the retirement you deserve. The best time to start saving was 20 years ago. The second best time is today.

Take a moment right now to view the graphic above and calculate how many paydays you have left before your target retirement age. That number is finite and diminishing. What will you do with them?