Site Search

Our site search facility enables you to look for content both within our main site and also our blog pages.

The first time a search is performed all pages are scraped for content which may take a few seconds to complete depending on your internet connectivity speed.

If you wish to search for a specific term or phrase please enable the 'ab' button within the search dialogue box

How long will your

savings last?

a year?

a month?

a week?

And then What?

Disability can cripple both your body and your finances

Be honest, could you survive financially if your income stopped due to illness or an accident?

Wouldn't you need a replacement disability income?

Unless you have readily available cash at hand, you may well be in a very vulnerable financial position without disability income protection insurance.

Long term illnesses and incapacity (such as cancer therapy treatments) can wreak havoc with family finances at a time when most can ill afford it.

Worries and stress, related to financial issues, are known to exacerbate medical conditions and hamper recovery creating a vicious cycle that can very quickly spiral out of control and into a mountain of debt.

Mortgages, housekeeping, school fees, loans and utility bills are just a few of the countless examples of expenses that continue when your income stops!

Why wouldn’t you protect your income?

Think about yourself and those that are financially dependant on YOU - your partner and your children - how would their lives be impacted if YOUR income stopped!

Don't wait until you become uninsurable or start suffering the consequences of financial hardship.

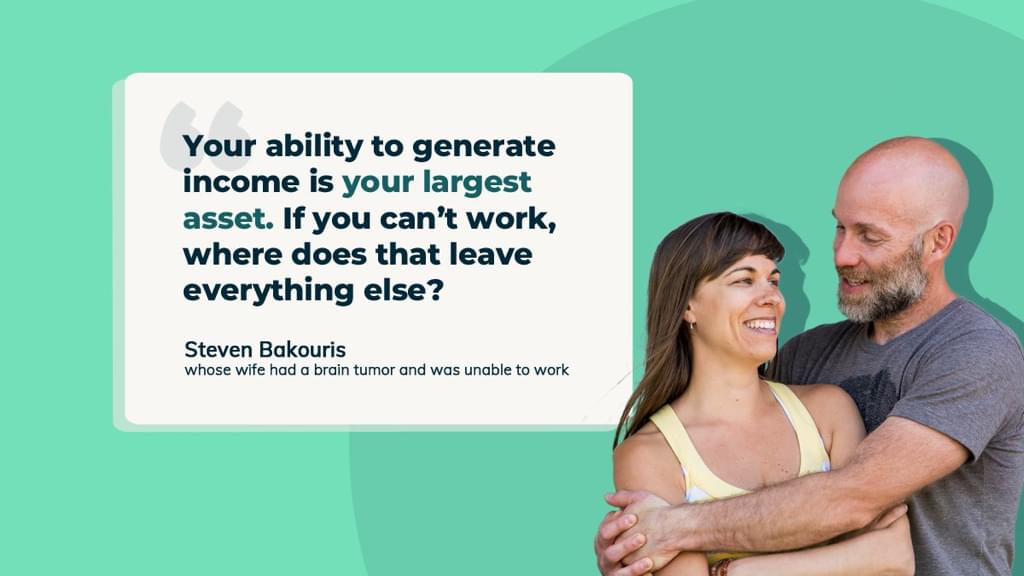

Claimant testimonials

Dean, Michael, Scott, Steven and Tim share their first hand experiences in each of their personal videos below of how their lives changed forever after sustaining life altering disabilities.

Many forget that becoming disabled can massively impact the lives of loved ones around them and the additional costs that they too often have to face whilst caring - read a first hand account of how 'Linda' and her family struggled after her road traffic accident

The law governs that we insure our motor vehicles, that are maybe worth USD 50K and yet the vast majority of people have never considered insuring their income.

OUR most important asset is our ability to earn income

Looked at another way, if you are currently aged 40 earning USD 50K per annum your potential lifetime income excluding pay rises, indexation etc up to age 60 will be a staggering:

USD 1,000,000.00

1 million dollars

How does disability income protection insurance work?

Once your disability income protection plan is effected, should you fall ill or become disabled, your income benefit payments will commence after your elected deferred period.

Your income payment benefits will continue until you return to work or, if you are unable to return to work, until your plan maturity date which is typically your 65th birthday.

Additionally, disability income protection benefit payments are subject to indexation to help keep pace with inflation.

How easy is it to effect diability income protection cover?

The following criteria is required to determine premium costs :

• your age

• your location

• your occupation

• your salary (a maximum level of 70% of pre-disability income is insurable)

• your chosen deferred period (this is the time between an accident or illness and the start of benefit payments, typically this would be 3 or 6 months)